Where we’ve been

Every year, the LGIS Board of Directors head out to one of our regional members, to see firsthand the excellent services and facilities local governments provide to their communities.

Portfolio Manager - Liability and Property

Udam has nearly 20 years' experience in insurance and risk management. Since joining LGIS, he has worked with WA local governments specialising in risk management and has served as account manager to a number of Scheme members. Udam now manages the Property and Liability portfolios of your Scheme. In this role, Udam is responsible for coverage, claims strategy, pricing and (re)insurance purchased by the Scheme to protect members.

The past year has thrown up many challenges, at home and internationally. Extreme weather events, bushfires, a global pandemic, just to name a few. Locally, we saw large parts of WA impacted by both fire events and significant storm and associated flood events. The recent Perth Hills bushfire was the largest bushfire event to occur in Western Australia since the Yarloop fire in 2016, which destroyed 180 properties.

Assets exposed to natural catastrophes – such as cyclone, flood, or bushfire – are bearing the brunt of the increases in the marketplace – especially those that experienced losses in those areas. Insured losses from major natural catastrophes in 2020 reached roughly US$78 billion, the fourth largest total since 2011 and about 17% higher than the ten-year average of $66.5 billion.

Many experienced insurance commentators are reporting we are currently in the midst of the most challenging market conditions of the past few decades, with all classes of insurance under significant pressure and a continuing hardening of the market across most sectors of the insurance market. In this climate insurers are more assertive in paring back coverage and limits and applying exclusions, which impacts our purchase of indemnity protection for the mutual.

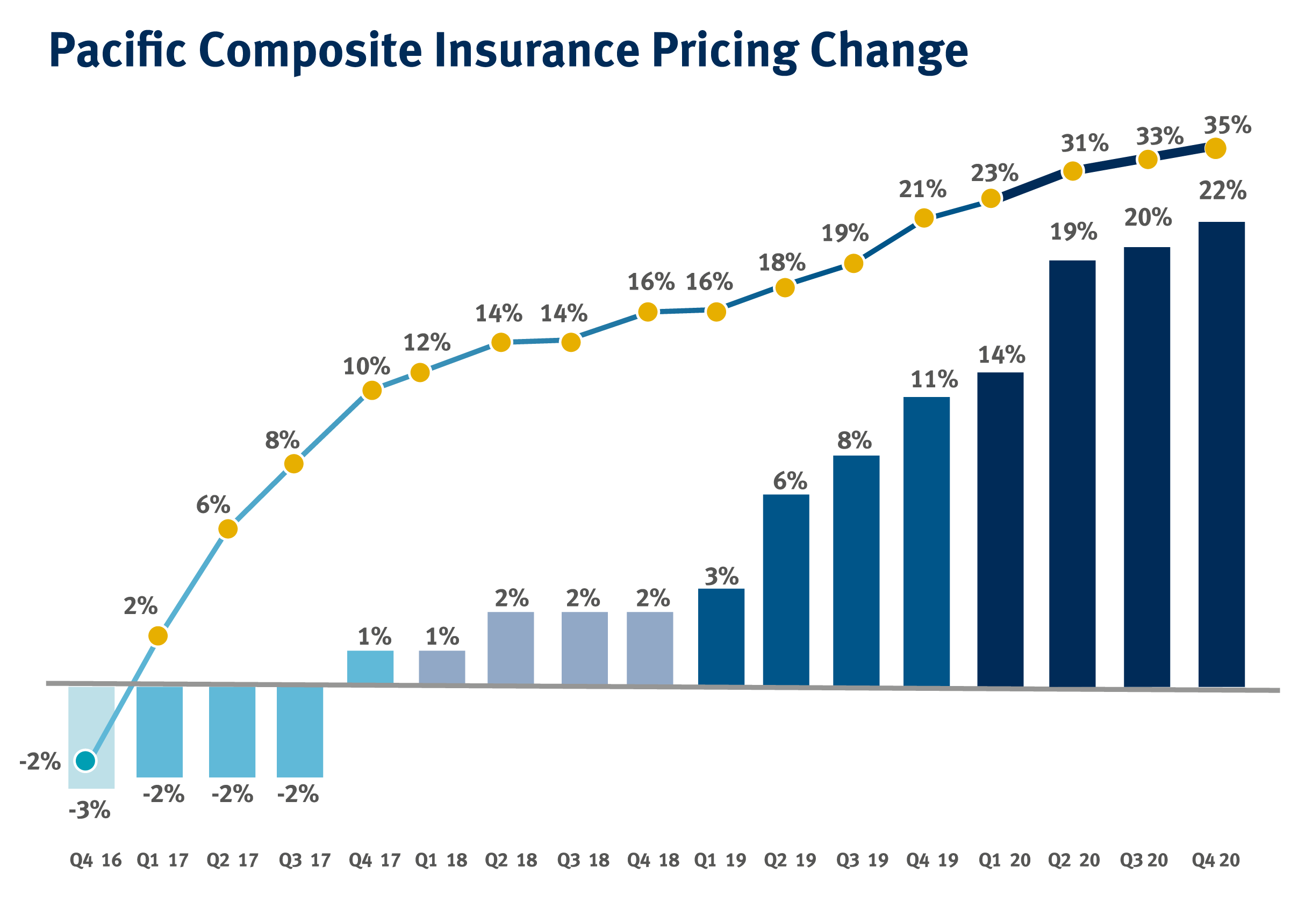

The Marsh Global Insurance Market Index – which measures its global commercial insurance premium pricing change at renewal and represents the world’s major insurance markets – reports that global commercial insurance prices rose 22% in the fourth quarter of 2020.

The increase, the largest since the index was launched in 2012, follows year-on-year average increases of 20% in the third quarter and 19% in the second quarter.

More specifically to Australia, the overall insurance pricing in the Pacific region increased 35% in the fourth quarter of 2020, continuing an upward trend that began in 2015.

Every year, the LGIS Board of Directors head out to one of our regional members, to see firsthand the excellent services and facilities local governments provide to their communities.

Installing the wrong furniture in the workplace can be a real pain the neck – or even the back or the shoulders.

The past year has thrown up many challenges, at home and internationally. Extreme weather events, bushfires, a global pandemic, just to name a few.

The current market environment is arguably not a “traditional” hard market. In a traditional hard market, capital – and consequently capacity – are reduced, limiting the availability of insurance. Our current climate feels more like an “underwriting driven” hard market, where (re)insurers are being forced to ensure they can deliver a profit from their underwriting going forward.

They need to get their combined ratios (Loss and Expenses) below 100% and not rely on investment income to make their profits. I n the current environment, (re)insurers are focused on technical assessment for risk and focus heavily on the quality and availability of data. The Scheme commenced a program to improve data quality over 2020 and this continues in 2021. A close look at the LGIS membership renewal declaration for 2021 will see increased scrutiny in areas of operations, aged care, child care, waste management, natural hazards, and building and planning activities.

While LGIS is not immune to the impacts on the wider insurance market (as we buy indemnity protection), we were fortunate to have been able to avoid many of these pressures and 20%+ increases. The risk-based approach we have taken provides the sector with a robust model to withstand the current environment.

While the general market conditions prevail across all protection classes, we anticipate the most significant impact being on Property, Liability (general, professional, cyber and management liability) and Bushfire funds.

Last quarter, commercial property insurance pricing increased 31%, similar to the quarter before, as the Australian market suffered heavy catastrophe losses in 2020.

A report published by a leading insurance actuary highlighted the ongoing poor probability with insurers’ combined ratios above 100% over the first half of the year and consistently above 100% for the past five years. All insurers are actively seeking to improve profitability with a number insurers signalling:

reductions in capacity (how much you can buy) / big jump in pricing +>25%

withdrawing from certain geographical regions

looking to remediate their accounts and remove risks that do not fit their appetite

focused on writing out asbestos and hazard material in buildings

The market conditions and the Mutual’s property claims record over the last two periods will place pressure on pricing through 2021. The Scheme has well established and long term indemnity providers who understand the stability required by the Mutual, and while we do expect increases, we are well positioned.

Similarly to property, general liability insurers continue to push pricing of liability risks in a manner where they can be underwritten sustainably over the cycle. It looks like it will take insurers several quarters of re-underwriting to overcome the challenges associated with the current marketplace, meaning prices will continue to rise and market coverage will continue to be restricted through 2021. We are aware of a number of entities engaged in waste, bushfire and planning (similar activities undertaken by local governments) that have seen +50% increases in price, reduction in limits and coverage withdrawal.

In fact, the Kimberley Land Council recently reported that indigenous ranger groups in the north of the state may have to stop their bushfire suppression work at the end of June due to fire insurance premiums more-than-doubling in the space of a year.

Other developments across claims arising from departmental inquiries, employment practises liabilities, and defamation action feed into the volatile performance of the management liability protection.

This year we have seen a general trend to better understand cyber exposure – events such as the solarwind intrusion to the more recent attempt in the US, where hackers remotely accessed the water treatment plant and briefly changed the levels of lye in the drinking water – are fuelling a need to better understand the risk, and importantly the protection deployed.

Significant weight is applied by the Mutual’s indemnity providers on risk management practices and controls implemented by members in addressing sector-specific exposures; evidenced by continuity and certainty in coverage.

In the current climate, the Scheme has been able to develop and deliver solutions to better insulate the Mutual from the changes faced in the general insurance world.

Whilst making up a small proportion of Scheme operation; the bushfire portfolio is the most volatile due to the cost, nature, and frequency of claims.

The requirement for this type of protection is unique to WA and is vital for members to meet their regulatory requirements. In 2020, the Scheme increased its pooled cover (self-insured retention) to improve the attractiveness of this portfolio to reinsurers and limit the impact on members. Given the limited pool of local indemnity providers prepared to write this business, the 2021 outlook will be challenging.

Despite these market cycles, your Scheme continues to deliver the best value for money in respect to the overall cost of contributions, breadth of cover, and specialist local government risk management support. By pooling member contributions, retention of manageable risk exposure and the evolution of Scheme protection as the local government risk profile evolves, the ‘hard’ insurance market is where the mutual Scheme comes to the forefront.

Therefore, while the commercial market has little appetite and ability to withstanding these increases, LGIS has made concerted efforts to limit contribution volatility.

We have developed our protection and (re)insurance structures over a number of years to reflect the complexity of local government and commercial insurers have not been able to match it. The Scheme transition to improve the breadth of protection available to members is currently in Phase 2 – further updates on what this means for members will be announced in April/May.

The LGIS model reduces the impact of global events and the expansion of the Scheme provides members with greater stability across a wider range of areas.

For more information on how market trends could affect you call your member services account manager.

Many WA local governments have waterways within their area, and must work together with other entities – such as the Department of Water, landowners, and state government agencies – to keep these waterways, and the people who visit them, safe.

When hiring a new staff member it is important to ensure they are able to perform the inherent

requirements of the role and have the required skills, qualifications (applicable to the level of the role) and knowledge to perform the role they are employed to do.

Psychological injury claims are expected to increase in 2021 with the ongoing stress of living through a pandemic.