Upcoming events – Spring 2023

Learn more about upcoming events and workshops that LGIS are taking part in.

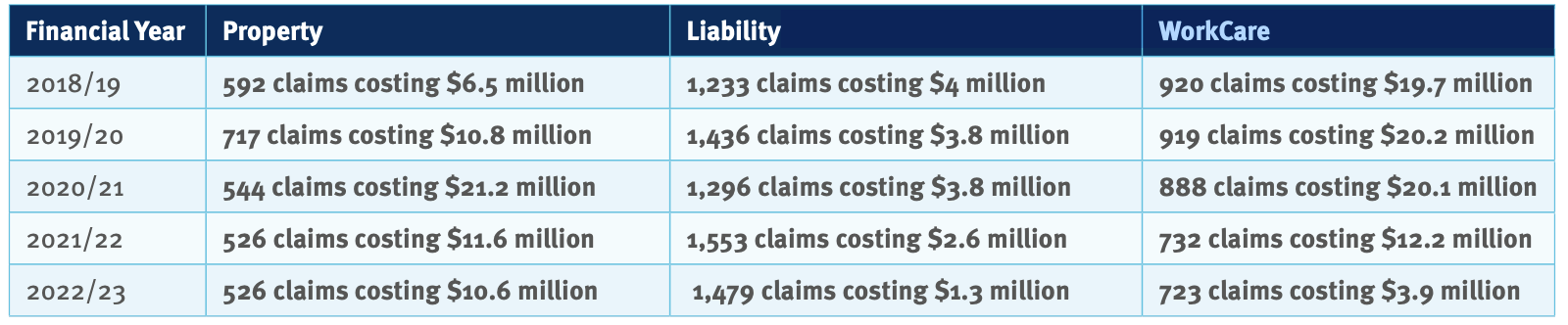

In 2022/23 LGIS received over 2,300 claims and paid out over $43.8 million. It’s a similar story most years with LGIS handling more than 2,000 claims across property, liability, workers’ compensation, motor and volunteer bushfire fighter protection.

An outside worker in his early 40s sustained a significant workplace injury to his lower back at a local government owned/ operated facility while trying to assist a ratepayer who had attended the facility.